Caleb Guilliams invited me on the BetterWealth podcast to talk about what most people get wrong about money.

We got straight to the point.

- What Infinite Banking really is.

- Why do most people misunderstand it?

- And how Nelson Nash used it to create generational wealth.

If you’ve heard about Infinite Banking but still aren’t clear on what it means or why it matters, this breakdown is for you.

Let me walk you through the highlights of our conversation in plain English.

What is Infinite Banking?

Infinite Banking is about understanding how money moves, how to take control of it, and how to stop giving away the banking function to someone else.

Caleb nods and says:

“Most people think it’s about insurance. But it’s really about thinking like a banker, not a customer.”

It’s about understanding how money flows in and out of your life and reclaiming that function so you are in charge.

Nelson used to say that banking is a process.

It’s the movement of money.

And every one of us participates in that process, whether we realize it or not.

So the question becomes:

Do you want to control the banking function in your life? Or give it away to someone else?

That’s the heart of Infinite Banking.

Caleb Guilliams pushes further. “But what does that look like in practice?”

Great question.

First, you must rethink your financial priorities.

- Stop asking “Where should I invest?”

- Start asking, “How much control do I have over my money today?”

Second, you recognize that savings and investing are not the same.

- Saving = control, access, liquidity.

- Investing = risk, reward, volatility.

If you don’t have capital saved first, investing is just gambling.

Finally, you implement a system that helps you build capital consistently.

For me and thousands of others, that’s a properly structured dividend-paying whole life policy.

Not because it’s flashy or complex. But it forces behavior change.

Premiums = forced savings.

Control = guaranteed access.

Tax-free growth and transfer = long-term peace of mind.

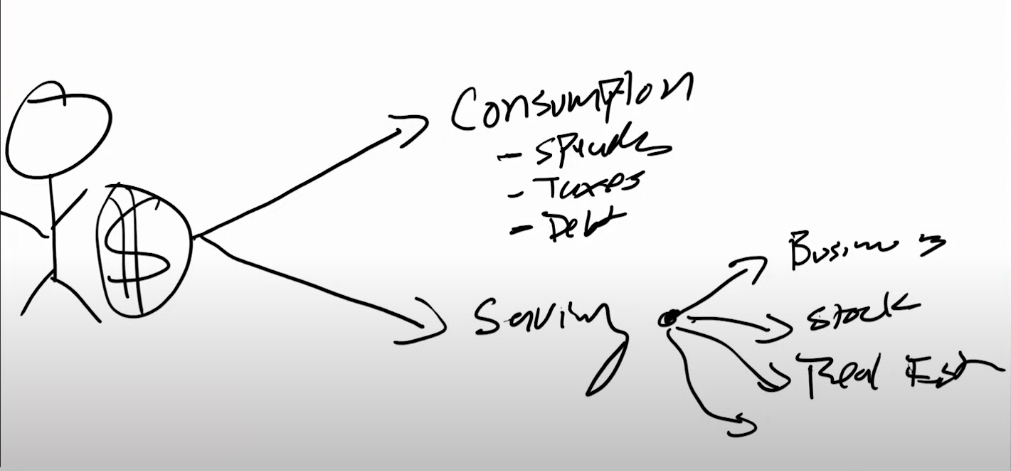

Caleb Guilliams draws it out on his whiteboard.

He shows two paths:

- Consumption

- Saving

He points out that most people are on Path #1: they consume almost everything they make.

Path #2 requires intention.

And as Caleb Guilliams says:

“When you choose to save more, your life changes.”

Brent Kessler is a great example. He went from saving zero to saving over $4,000 a month once he adopted the Infinite Banking mindset. That one change completely altered his financial direction because he finally had a system and a reason to save.

Why Consistency Matters More Than Products

Too many people chase the product.

They think if they get the “best policy design” or the “highest early cash value,” they’ll win.

That’s short-term thinking.

Nelson didn’t build wealth that way.

He built it with patience.

With intention.

With 45 policies and zero dependence on traditional banks.

When Nelson passed, 17 of his policies paid a tax-free death benefit to his family. The other 28 policies continued to live on, building value and providing control for future generations.

That’s real Infinite Banking.

Nelson applied these principles in his everyday life. He used policies to fund real estate, business, and family needs. His actions showed how the Infinite Banking Concept works beyond theory.

The Real Risk Isn’t the Tool but the User

In our conversation, I shared one of my favorite analogies:

A properly designed whole life policy is like a chainsaw. It’s powerful but dangerous if misused.

If I hand you a running chainsaw and say “go for it” without showing you how to use it—someone’s getting hurt.

That doesn’t make the tool bad. It just means the user isn’t ready.

The same is true for Infinite Banking. What matters most is how you think about money and behave with it daily.

As Caleb Guilliams said, “You can’t spreadsheet your way out of bad behavior.”

We both agreed that many people misunderstand what Infinite Banking really is. The focus is on learning how to manage your money with purpose.

Even Dave Ramsey agrees that behavior matters.

This surprised some people, but Caleb brought up a point I agree with: Dave Ramsey’s system works for millions because it’s behavior-based.

His famous 15-year mortgage strategy? It works because it helps people stay consistent and avoid unnecessary financial mistakes.

Same with cutting up credit cards.

Infinite Banking does the same thing—only with more control, more liquidity, and more long-term flexibility.

If you pay your insurance premiums like clockwork, you’re essentially saving consistently. That’s powerful.

What Nelson Nash Actually Did—Not Just What He Taught

Nelson followed what he taught. He used the system every day to fund real purchases and real goals.

He financed real estate deals, bought airplanes, and paid cash for cars, all through policies.

He never had to go begging to a bank for permission.

And when he died, his family didn’t just get death benefit checks, but inherited systems that continued building wealth.

I shared this on the podcast:

“Imagine you have 45 rental properties, all paid off, all producing income. That’s how Nelson built his system—using life insurance policies to play the role most people assign to rental properties.”

And here’s something most people don’t realize:

Some children today are uninsurable.

I’ve had the heartbreaking job of telling parents they can’t get a policy on their kid because of health or behavioral issues.

You never know what your insurability window is.

The best time to get started is always yesterday.

The next best time is now.

Saving vs Spending: a Mindset Shift

We also touched on how people misunderstand what it means to “pay yourself back.”

If you borrow against your policy to pay off a credit card, you don’t get ahead unless you repay your policy the same way you were repaying the bank.

If you were sending Visa $1,000 a month, why not redirect that to your own system?

As I said to Caleb:

“Who do you value more—Visa, or your family?”

That shift—from spending to saving, from giving to banks to giving to your future—that’s the engine of this process.

And that’s why we structure policies the way we do.

- To create forced savings.

- To create liquidity.

- To create ownership.

Final Thoughts

Here are five key takeaways from my conversation with Caleb Guilliams:

- Infinite Banking is about taking control of the banking function in your life, not chasing the best insurance product.

- Saving must come before investing. Without capital, you’re just gambling.

- Tools like whole life policies are only effective if paired with disciplined behavior.

- People like Brent Kessler and Nelson Nash succeeded because they changed how they thought about money.

- The earlier you start, the more options you create for your future—and your family’s.

To wrap up, Caleb and I kept coming back to one thing: savings.

Building consistent savings gives you options.

If Infinite Banking helps you do that with structure and discipline, it’s worth considering.

Want to go deeper?

Read Don’t Spread the Wealth.

It will challenge how you think about money and help you take real ownership of your financial life.

Related Reading

- Kyle Fuller on how the Infinite Banking Concept Changed My Life and Built a $650 Million Legacy

- David Stearns on building Generational Wealth with the Infinite Banking Concept

Ready to Put This Into Practice in Your Own Life?

If this conversation gave you a clearer picture of how Infinite Banking can work for a Canadian family or business, the next step is simple. I help families design and run policies that fit their actual cash flow, business structure, and long-term goals. We do not start with the policy. We start with the plan.

If you would like to walk through your own situation with me, book a no-pressure conversation at coachcanfield.com. We will look at where your money is actually flowing today and what an Infinite Banking strategy could change about that.